ZeroHedge - On a long enough timeline, the survival rate for everyone drops to zero

www.zerohedge.com

Wall Street Wins Again: Banks Force Treasury To Double Rate On Small Business Rescue Loan

Fri, 04/03/2020 - 05:29

Update (1800ET): And so Wall Street wins again.

After we warned earlier that the SBA's $350BN Paycheck Protection Program, which is expected to be launched at midnight tonight and is meant to bailout America's small and medium business (<500 employees), may never even get off the ground because the proposed interest rate on the loan of 0.5% is too low lender banks (alongside with various other considerations as listed below) with JPM saying it “will most likely not be able to start accepting applications on Friday, April 3rd as we had hoped", in a press conference late on Thursday,

Steven Mnuchin said that he will double the interest rate on the SBA loan from 0.50% to 1.00% in order to appease banks seeking higher interest rates to participate in the Treasury's bailout program and lend money to the same taxpayers who bailed them out 12 years ago.

These are same banks, mind you, that just sold all $1.6 trillion in securities to the Fed to expand their balance sheets capacity in the past three weeks, and which also just benefited from the Fed's decision to remove Treasurys and deposits from the Fed's SLR test, freeing up another $1.6 trillion in liquidity.

Furthermore, these loans

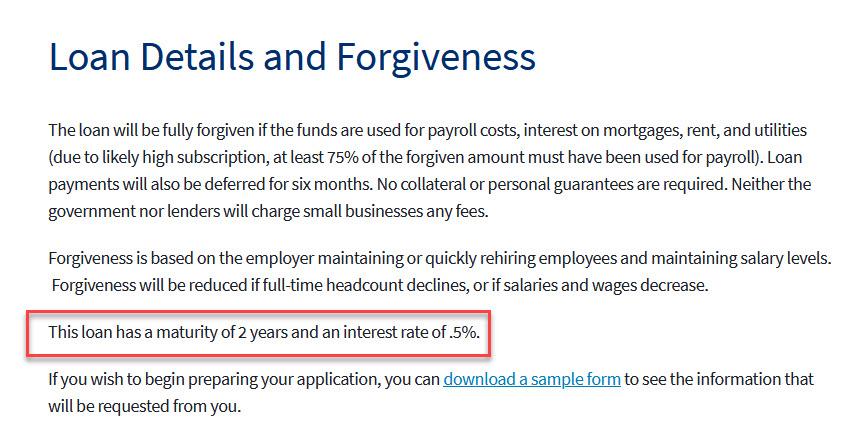

are guaranteed by the federal government and don’t require collateral, and will be forgiven if funds are used for payroll costs, mortgage interest, rent and utility payments for two months and if businesses retain and rehire employees.

So bank don't take any risk - why are they charging any interest at all, or rather why do they have any say in what the rate should be?

And yet, despite all this, these banks - which include JPMorgan Chase, Bank of America, Wells Fargo Citigroup, Truist Bank and PNC - which were bailed out in 2008 and again bailed out 3 weeks ago with the Fed's various alphabet soup programs, couldn't agree to give Main Street a helping hand, and instead of offering loans at a modest 0.5%, demanded no less than 1%, which is 75-100 bps above where they can borrow cash from the Fed. Because charging America's middle class a record 17%

credit card interest rate is not enough, and anything less than 1.0% on a loan that is explicitly backstopped by the Treasury would be uneconomical.

A senior administration official told reporters on Tuesday there could be millions of applications when the program goes live on Friday, with the idea funds would be disbursed quickly, even the same day, on a first-come, first-serve basis. But lenders complained it wouldn’t be possible to process the loans that quickly without having more guidance from SBA, and they were awaiting more information.

Finally, we have a question:

who the hell calls the shots here - the perpetually insolvent banks, who would be in dire straits had it not been for the Fed's now trillions in excess reserves, and

which once again steamrolled over Main Street, or the Treasury which until

today had indicated a rate of 0.50% on the PPP loan...

... and which folded like a cheap seat as soon as the banks demanded another pound of taxpayer flesh, and doubled the rate to 1.0%. In fact, we hope someone finally asks former Goldman Sachs partner Steven Mnuchin on whose side he really is?

Update (1715ET): With just a few hours before the expected launch of the federal program to dole out at least $350 billion in loans to small businesses (the Paycheck Protection Program),

CNBC's Wilfred Frost reports that JPMorgan Chase, the biggest U.S. bank, emailed customers late on Thursday to say

the company “will most likely not be able to start accepting applications on Friday, April 3rd as we had hoped.”

However, Frost goes on to say that the bank makes clear that

they are doing all they can to be ready as soon as possible.

* * *

Tonight at midnight, the most critical - if hardly biggest - part of the Fed's $2 trillion fiscal stimulus is expected to begin: that's when small and medium business with 500 employees or less can request a loan of up to 2.5x the average monthly payroll (capped at $10 million), meant to buy cash-strapped companies just under 3 months in liquidity. As we discussed previously, the loans which are packaged under the SBA's

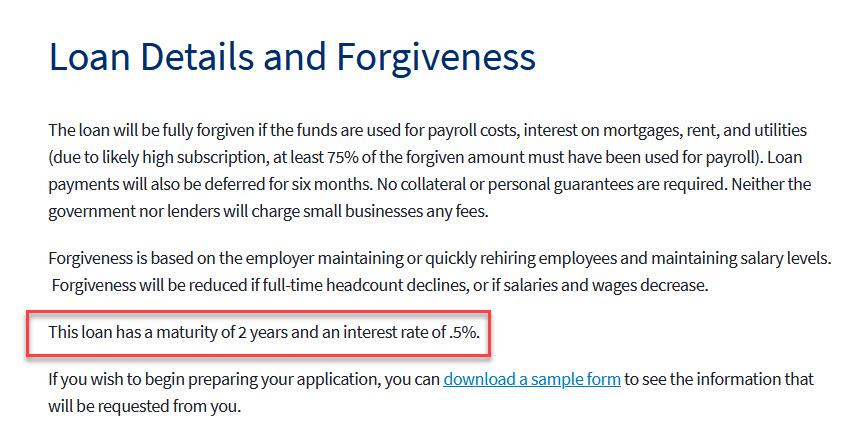

Paycheck Protection Program carry a 0.5% interest rate, and would be forgiven if their proceeds are used toward operational uses such as payrolls, utilities, and rent.

Needless to say, getting these loans into the hands of America's 30 million small businesses is absolutely critical:

they employ about half of U.S. private sector employees, according to the Small Business Administration website.

There is just one problem:

with just hours to go until millions in small businesses across the nation scramble to apply for much needed funding, the program appears to be on the verge of collapse amid what appears to be sheer chaos between the Treasury, the Small Business Administration, and the various commercial banks that will be tasked to loan the action money.

One reason why the program is woefully unprepared for a Friday midnight rollout is that banks that haven't underwritten SBA loans before will need to get onboarded in the system. However, as Politico reports, as of last night,

there was no application available for banks to do this, and as CNBC's

Kayla Tausche adds, Treasury remains committed to originating these loans beginning tomorrow, despite hiccups.

But wait there's more: as CNBC's Kate Rogers reports, an "official familiar with the Paycheck Protection Program loans rolling out tomorrow says official guidance for banks is not yet finalized" with Kayla Tausche adding that in addition to general guidance, banks are asking Treasury for two specific changes to the small biz program:

- Smaller banks want higher interest rate so they don't lose money

- Big banks want "know your customer" rules waived so they can lend to co's they haven't worked with

In addition to general guidance, banks are asking Treasury for two specific changes to the small biz program:

- Smaller banks want higher interest rate so they don't lose money

- Big banks want "know your customer" rules waived so they can lend to co's they haven't worked with

— Kayla Tausche (@kaylatausche)

April 2, 2020

Meanwhile, with the supply side choked off amid last minute rollout chaos, demand for the bailout cash is exploding with some estimates that as many as $1 trillion in loan requests will be available for the $350BN in "first come, first serve" loans. As Tausche adds, "industry sources say a "feeding frenzy" of small biz demand for limited resources will be problematic for the system, technically" and notes that "executives are preparing for a situation akin to the 2013 roll-out of

http://Healthcare.gov"

That, for those who may not recall, was an unmitigated disaster lasting for months.

But while logistical issues will be overcome, a potential dealbreaker of a problem is that the physical source of new loans is getting cold feet.

According to Reuters,

thousands of U.S. banks, including some of the country’s largest lenders, have said they may not participate in the federal government’s small-business rescue program due to concerns about taking on too much legal and financial risk.

While the Trump administration has said it wants the loans disbursed within days, bank representatives, as well as thousands of community lenders,

have expressed serious reservations about participating in the scheme in its current form and called that deadline totally unrealistic.

Their biggest concern is that the Treasury Department said on Tuesday that lenders will be responsible for preventing fraudulent claims by verifying borrower eligibility, which is determined by a few measures including the borrower’s number of employees and its average monthly payroll costs.

That's not all: banks also must take steps to prevent money laundering and terrorist financing, a process that would normally take weeks, the sources said. Additionally, banks are concerned they could face regulatory penalties or legal costs down the line if things go awry in the haste to get money out the door.

But at the same time they are worried they will be blamed for not moving funds fast enough if they perform due diligence the way they would under normal circumstances, the sources said.

Then there is the mandated interest rate on the loans:

community banks said the Treasury’s guideline interest rate of 0.5% will be unprofitable, and that many small banks will not have sufficient liquidity to front up the loans (this, as we said yesterday, may have been a primary consideration for the Fed to release Treasuries and deposits from the Supplementary Leverage Ratio test, effectively opening up over $1 trillion in additional loan capacity across the US banking sector).

"Taking all of the above concerns into consideration, many banks have already indicated that they will not be able to use the Program under the current terms,” the Independent Community Bankers of America wrote to the U.S. Treasury and Small Business Administration, which are jointly administering the loans program, on Wednesday.

“We strongly recommend that you make changes to the guidelines before the Program goes live so that it will work as intended by Congress,” the group, which represents thousands of small banks across the country, wrote.

Alas, that is impossible as going back to the drawing board would mean days if not weeks of additional delays, which for an economy where every hour matters, is simply not feasible..

Still, as Reuters reports, as of late Wednesday night, after hearing the concerns, Treasury officials are considering withdrawing Tuesday’s guidance and are working to fix the issues, although as of this moment the same guidelines for the PP program were still in place as earlier this week.

Banks also want a document customers can sign attesting to their eligibility and other requirements, thereby relieving the industry of responsibility for potential misconduct.

One source said banks are also seeking a written assurance from the government regarding their legal liabilities and obligations before they agree to participate in the program.

Reuters could not learn which specific big banks are thinking about shunning the program. The Bank Policy Institute (BPI), a Washington trade group, hosted a call on Wednesday during which executives from its members discussed their concerns, three of the sources said. Members of the group include

JPMorgan Chase, Bank of America, Wells Fargo Citigroup, Truist Bank and PNC.

“Our banks are committed to ensuring this program works and that all of the operational complexities and process challenges are worked through so we can achieve Congress’s goal of helping America’s small businesses,” Greg Baer, President and CEO of the BPI, said on Thursday.

Which is ironic: back in September 2008 all the banks demanded multi-trillion taxpayer funded bailouts right this instant as the world was going to implode if a few banks went under. However, now that the tables are flipped, and mainstream America and half of all the private sector employees demand a similar turnaround time or else the US economy will truly collapse, banks suddenly think that taking their time, dotting i's and crossing t's is far more important than getting money into the hands of America's workers. Money which, as a reminder, is now of the "helicopter" variety, openly printed by the Treasury, monetized by the Fed, and which can be delivered to banks through the back door if need be.

With that we look forward to seeing how this chaos resolves itself, and the unprecedented anger that will erupt if US banks - so generously bailed out in 2008 - are the gating factor to getting the critical $350BN in relief loans to America's small business.

For those who are confident this story will have a happy ending, here is a

twitter thread from Brock Blake, the CEO of Lendeo - a small business loan marketplace - who explains succinctly why there is no way this program can possibly roll out tonight:

Wow. What a mess! Just got off a conf call with the SBA. The @SBAgov & @USTreasury are having a power struggle and this is turning into a disaster. Millions of small businesses will be lining up for loans tomorrow, yet those 2 organizations are fighting about process & forms.

Treasury releases an app for the PPP loans and the ENTIRE country has been filling it out in preparation for tomorrow. Our engineers have been working for 48 hours straight to build an automated experience... and now, the SBA is saying that THAT application is not complete!

It’s 12 hours before America’s small businesses will be applying... and they STILL haven’t released a new app for lenders.

**There’s no way this will be ready by tomorrow.**

No one actually knows what’s needed to actually document the application. There’s been no updated guidance from the few documents they posted on Monday. At this point, there are WAY more questions than answers.

Lenders are begging to get answers like:

- does the bank have to be an SBA-licensed lender to participate? Or just an FDIC bank?

- how does a lender apply to approved as a PPP lender? On Monday, the guidance said to just send an email to apply, but SBA is saying that’s not correct. The lender needs to complete a new expedited ‘750 application.’

I asked when they would release the application (because many lenders are waiting response to the email they sent. SBA’s answer: soon!

- most lenders are worried they won’t have enough capital to fund the demand, and are asking how quickly they will be ‘reimbursed’ on the loans so they can replenish capital. No answers yet.

- while the low rate is exactly what the SMBs need, many lenders are opting out of the program because they can’t make enough $ to even service the loans (0.5% per year is VERY skinny).

- 30m small businesses will be beating down the doors for capital tomorrow ... its a DISASTER waiting to happen.

BOTTOM LINE: the SBA & the Treasury need to quit the power struggle, get aligned, provide REAL guidance (for ALL lenders, business owners, and agents) so that we can get much need capital into the hands of

Finally, here is a recap of key issues ahead of the imminent PPP rollout courtesy of CNBC's Tausche.

$350 billion of small business loans will be made available tomorrow, but is the government ready to roll out the program?

@kaylatausche has the details on bankers' concerns that the program is not ready for prime time on

@CNBC.

pic.twitter.com/fmheeBTNmE

— The Exchange (@CNBCTheExchange)

April 2, 2020

")